CSRD Topical Standard ESRS S3: Why All Companies Need to Assess Proximity to Affected Communities

Key Takeaways

While ESRS datapoints have been consolidated, companies still need to assess proximity to affected communities

The only accurate way to assess materiality of potential impacts to affected communities is through a location-based, bottom-up approach

If you use any natural resources (such as land or water), your sites should be screened for Indigenous Peoples in the area, as they can be affected by your company’s actions

We recently wrote about the new draft ESRS E4 regulation, released in July 2025, and its implications for reporting on biodiversity and ecosystems. In this article, we focus on the draft Topical Standard ESRS S3: Affected Communities.

Background

The Omnibus Simplification Package, released in February 2025, is a set of proposals aimed at streamlining and simplifying sustainability reporting requirements in the EU, including the Corporate Sustainability Reporting Directive (CSRD)’s ESRS. The goal of the Omnibus is to reduce the administrative burden on companies, particularly SMEs, while enhancing the EU’s competitiveness and facilitating the transition to a sustainable economy.

EFRAG is the technical advisor to the EC and was appointed to develop the initial ESRS. EFRAG was mandated by the EC to revise and simplify the ESRS and improve their overall usability.

On July 31, EFRAG released its “exposure draft,” which is available for public consultation until September 29, 2025. The new simplified set of ESRS reduces data points by 57% while preserving its core objectives.

With the final draft expected to be completed in fall 2025, EFRAG advises companies that are in scope to get started on their double materiality assessments (DMAs), as the topics for materiality haven’t, and won’t, change.

Changes to the ESRS requirements: Affected Communities

One major change that was made in the general draft requirements is to strengthen the role of materiality as a general filter for all reported information. Companies are not required to disclose any information on environmental, social, and governance topics covered by ESRS if they have assessed the topic as non-material. The aim is to reduce the reporting burden and encourage more concise disclosures by eliminating the requirement to report on non-material items.

Regarding Affected Communities, there are relevant aspects in the General Requirements (ESRS 1), General Disclosures (ESRS 2) and Topical Standard ESRS S3, Affected Communities. While many ESRS datapoints have been cut or consolidated, the fundamental concept of assessing business activities for their potential impacts to Indigenous Peoples or local communities remains. This may not seem intuitive in reading through the draft regulation- so here we break it down for you.

While many ESRS datapoints have been cut or consolidated, the fundamental concept of assessing business activities for their potential impacts to Indigenous Peoples or local communities remains.

Double Materiality Assessment and Overview of Approach to Regulation

ESRS 1 notes that companies may adopt either a top-down or a bottom-up approach to perform the double materiality assessment (AR 17 for para. 48(a)). While top-down is allowed, there is one aspect of assessing impacts to affected communities that, to fully meet the spirit of the regulation, requires a bottom-up approach: proximity of business locations to Indigenous Peoples and local communities.

One of the purposes of the ESRS topical standards is to understand where and how your company is having an impact on the environment and people. Because impacts to communities and to nature are inherently location-specific, the only way to assess these impacts is through a bottom up approach: by analyzing which communities (ESRS S3) or what kind of biodiversity and nature (ESRS E4) are located close enough to your facility that you may have a potentially negative impact on them. Using a top-down approach may fail to uncover these risks, leaving your company exposed to both legal risk and compliance risk.

To have an audit-proof, defensible, good citizen approach, you need to conduct your DMA from the bottom up. This is easily done via a platform like ours at Dunya Analytics, which includes an assessment of the proximity of business locations to potentially Affected Communities. In fact, our customers have been surprised to learn that they were unaware of some communities living in proximity to their business sites.

The Details

Here we provide the specific language in ESRS 1, ESRS 2, and ESRS S3 that apply to Affected Communities.

ESRS 1- General Requirements

ESRS 1 lays out the fundamental principles for sustainability reporting, including the role of affected stakeholders and communities.

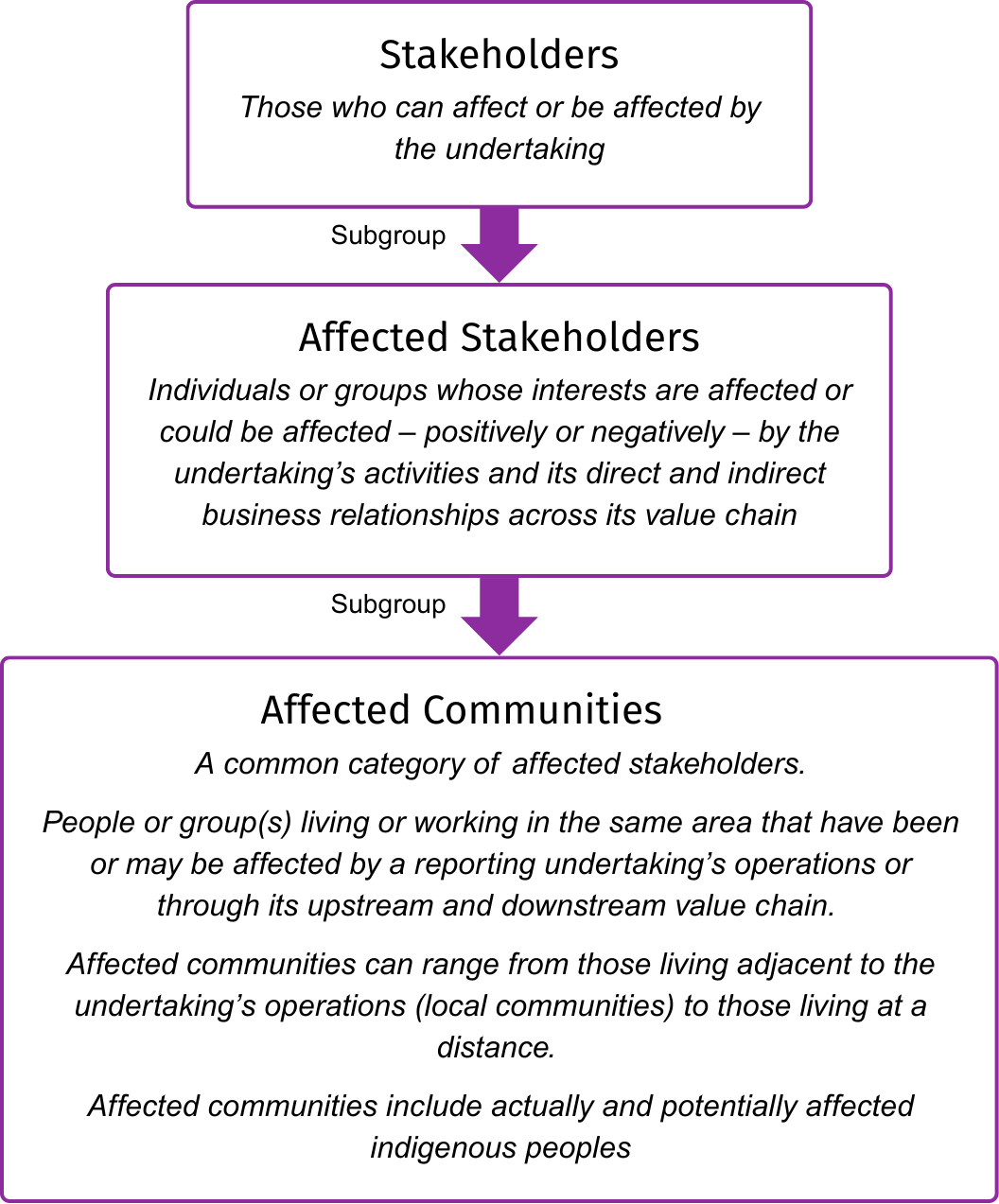

Double Materiality Assessment Input: ESRS 1 explicitly states that "The results of the engagement with affected stakeholders provides a key input to the impact materiality assessment. Common categories of affected stakeholders are: employees and/or workers' representatives, suppliers, consumers or end-users, affected communities and persons in vulnerable situations.” Definitions of Stakeholders, Affected Stakeholders, and Affected Communities are as follows (Paragraph 33 and Annex II):

Note that the definition of affected communities includes “potentially affected Indigenous Peoples.” This implies that if you are using any natural resources (such as land or water), your sites should be screened for Indigenous Peoples in the area, as they can be affected by your company’s actions.

ESRS 2- General Disclosures

ESRS 2 details the general disclosure requirements, many of which involve affected stakeholders and communities.

Process to Identify and Assess Materiality (IRO-1): ESRS 2 requires disclosure of the process to identify and assess material impacts, risks, and opportunities. A key component of this process is "whether and how the process includes consultations with affected stakeholders and external experts to understand the impacts."

Phasing-in Provisions: For companies below a certain employee threshold (750 employees), if they choose to omit certain topical standards for the first two years, they "shall nevertheless disclose whether the sustainability topics covered respectively by ESRS E4, ESRS S1, ESRS S2, ESRS S3 or ESRS S4 have been assessed to be material" (Paragraph 6). This directly references ESRS S3 Affected Communities as a distinct topic subject to materiality assessment.

Topical Standard ESRS S3: Affected Communities

This entire standard is dedicated to providing comprehensive disclosure requirements related to affected communities, concerning their "economic, social and cultural rights (land-related impacts, security-related impacts, adequate housing and food, water and sanitation)", and other rights.

Companies are only required to report on ESRS S3 if the topic is deemed to be material. However, in this case, materiality is location-based, determined by whether business locations are in proximity to Indigenous Peoples and local communities.

When it comes to assessing impacts on affected communities, there is no substitute for a location-specific, bottom-up approach. If your company relies solely on top-down assessments, you are opening yourself up to significant risk—you may miss Indigenous Peoples and local communities in your business footprint, exposing yourself to legal liability, regulatory penalties, and reputational damage. In a principle-based regulatory environment like the EU, good intentions aren't enough—you must demonstrate that you've actually looked at your operations. The communities you don't know about are the ones most likely to become your biggest risk.

Here are the steps to take:

Screen for community presence (available on the Dunya Analytics platform)

Assess potential impacts (available on the Dunya Analytics platform)

Learning more about nearby communities and starting outreach where it makes sense

Timeline

The draft standards are open for public consultation, which closes on September 29, 2025. However, given that the updated ESRS E4 Standard better aligns with major frameworks such as the TNFD, it seems unlikely that the requirements will reduce in scope. Now is a good time to start understanding the metrics requirements and collecting your company’s relevant data.

Not sure how to navigate these CSRD communities disclosure requirements? Our solution at Dunya Analytics is the fastest way to get started measuring affected communities, nature and biodiversity, and easily understand your potential material impacts. Contact us to learn more about our CSRD compliance solutions.