Navigating the ESRS E4 Disclosure Requirements

Updated July 2026

For insights about the general ESRS requirements for Double Materiality Assessment and material topics, see ESRS DMA: Aligning Your Nature Risk Assessment with the CSRD.

The final draft of the ESRS was adopted by the European Commission in July 2026, and will enter into force in Q4 of 2026. In this article, we focus on how to meet the requirements and get the most value out of the ESRS Topical Standard E4, Biodiversity and Ecosystems.

The overarching goal of the Disclosure Requirements for ESRS E4 is to understand how a company is contributing to the nature-positive transition described in the Kunming-Montreal Global Biodiversity Framework (GBF), a historic agreement adopted by 196 countries in 2022 to halt and reverse global nature loss.

Is biodiversity material for your business?

The first step is determining whether biodiversity is a material topic to the business and thus required to be included among disclosures.

Double Materiality Assessment as it Relates to Biodiversity and Ecosystems

The final draft ESRS allows for flexibility in a company’s approach to double materiality assessment (DMA). Either a top-down or bottom-up approach can be used as long as material impacts, risks, and opportunities (IROs) are appropriately identified and disclosed. The ESRS describe that context is particularly important for biodiversity and ecosystems. If material impacts, risks or opportunities relate to specific geographies, then “it is important to consider appropriate aggregation or disaggregation of the reported information” such as by site or ecosystem.

If biodiversity is potentially material, then a location-based biodiversity materiality assessment must be done to identify what must be disclosed under E4.

For a comprehensive explanation of DMA compliance, see our insight: ESRS DMA: Aligning Your Nature Risk Assessment with the CSRD.

Conducting a location-based biodiversity materiality assessment

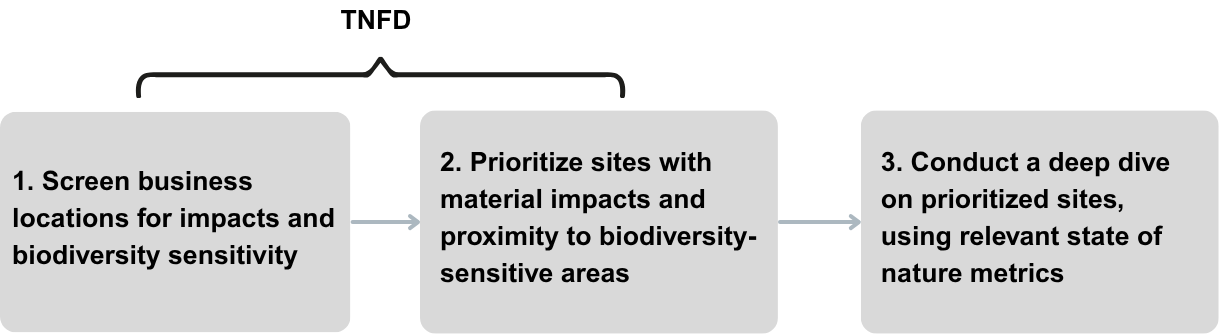

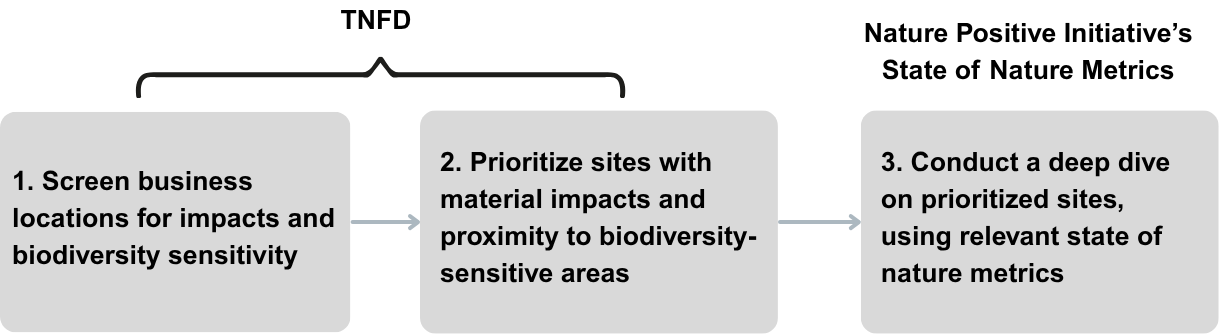

The ESRS recommends using the LEAP approach from the Taskforce on Nature-Related Financial Disclosures (TNFD) to assess materiality and uncover location-based IROs. The benefit of the LEAP approach is that it supports materiality assessment while also revealing the information needed in the next step in the disclosure: metrics related to biodiversity and ecosystems change.

If biodiversity is material, what information should be included in disclosures?

The purpose of the Disclosure Requirements within ESRS E4 is to understand how a company is performing against its material impacts, risks and opportunities related to biodiversity and ecosystem change.

Geographic scope

If biodiversity is found to be material, companies need to disclose the following material information regarding geographic scope:

a. Locations within the company’s own operations to which the material impacts, risks, or opportunities relate

b. For those locations, a list of “biodiversity-sensitive” areas that are related to the company’s material negative impacts

c. A list of the company’s activities related to negative impacts on the identified biodiversity-sensitive areas

This information can be determined using the LEAP approach.

Aggregating data

Companies are not necessarily expected to provide a complete list of all of their individual business locations and associated information. Information can be aggregated based on:

the nature of material impacts, risks, or opportunities,

the similarity of sites or affected areas,

the same biodiversity-sensitive area,

or other groupings, as long as the aggregation does not “obscure material information.”

Definition of “biodiversity-sensitive area”

The ESRS defines “biodiversity-sensitive areas” as:

Legally and otherwise protected areas, including:

Natura 2000 network of protected areas

Other protected areas, with the World Database on Protected and Conserved Areas (WDPCA) being the most comprehensive source

Areas that are scientifically recognized for their importance for biodiversity, including:

Key Biodiversity Areas (‘KBAs’)

Ecologically or Biologically Significant Marine Areas (EBSAs)

Habitats of species listed in IUCN Red List of Threatened Species (which are scientifically recognized for their importance for biodiversity)

Some of these datasets are freely available, while others require a paid license for commercial use.

How to determine material sites – material negative impacts in a biodiversity-sensitive area

ESRS E4 describes that if a business site “is in or near a biodiversity-sensitive area, its activities can be related to material negative impacts on the biodiversity-sensitive area.” Two factors determine if a specific business site is related to negative impacts on biodiversity-sensitive areas:

(1) the types of activities that are occurring at the business site

(2) the proximity of the site to the sensitive area

What proximity is considered “near”? The leading guidance on how to select the appropriate proximity for assessing a business site’s impacts is the Integrated Biodiversity Assessment Tool’s (IBAT) definitions for buffer zones. A buffer zone is the area assessed for the presence of any of the types of sites listed earlier in the definition of biodiversity-sensitive area.

Generally speaking, industries with activities known to have larger negative impacts should use a larger buffer zone than those with smaller impacts. For example, an agricultural site with high water and fertilizer use will have a bigger impact on species and ecosystems than an office building. According to IBAT’s guidance, an agricultural site would use a buffer of 10 km, while an office building would use a smaller buffer of 5 km.

Disclosure metrics required for material sites

The ESRS requires more detailed reporting to understand the nature of IROs at material sites using the following sub-topics:

(a) drivers of biodiversity and ecosystem change,

(b) the state of species (such as related to extinction risk),

(c) the condition and extent of terrestrial, freshwater, and marine ecosystems (such as related to site condition and landscape condition), and

(d) ecosystem services.

For site metrics, the ESRS align with guidance from the TNFD and the Nature Positive Initiative’s draft State of Nature metrics, expected to be finalized by the end of 2026. Companies can refer to those frameworks for methodology to support ESRS E4 compliance for these aspects of the process:

SFDR classifications

The ESRS require negative impacts be classified based on categories that align with certain SFDR Principal Adverse Impact (PAI) indicators, specifically whether they:

contribute to land degradation, desertification, or soil sealing

affect threatened species or ecosystems

Value chain

Companies need to disclose information on their value chain, specifically how their policies support the “traceability of products, components and raw materials that have actual or potential material impacts on biodiversity and ecosystems in its value chain.” This includes whether sustainable land practices, sustainable ocean practices, and deforestation have been addressed.

If you don’t have location data for your suppliers, check out our insight on Assessing Nature Risk in the Supply Chain with the Data You Already Have. It is understood that many companies do not have the locations of all of their upstream and downstream players. The Standards recognize that data availability will improve over time, and subsequently sets the expectation that value chain assessments should also improve over time.

Timeline for CSRD reporting

The draft ESRS are expected to be finalized and become legally binding in Q4 of 2026. These would apply for reporting on the 2027 financial year (with reports published in 2028), though companies may adopt them any time.

Why Start Now

Due to the complexity of nature topics, it typically takes companies three years to reach a level of confidence where they are ready to report on material nature topics. A basic assessment in the first year helps build fluency in nature risk and identify areas of measurement focus. A full TNFD assessment in the second year uncovers the comprehensive risk picture, enabling the first deployments of nature insights across the business. Expansion of the assessment to the supply chain and the development of nature targets and action plans happens in the third year, with companies positioned to publish regulatory-compliant nature risk disclosures.

Streamlining Your ESRS E4 Compliance with Dunya Analytics

Understanding the requirements is one thing, but efficiently meeting them is another. At Dunya Analytics, our platform is built to ease the challenge of location-based assessment – both for your direct operations and supply chain.

The ESRS references the first three steps of the TNFD LEAP approach, which our platform automates:

Locate interfaces with nature

Evaluate the related impacts and dependencies on nature

Assess your associated risks or opportunities

Our platform handles the technical complexity of data collection and geospatial analysis, so you can focus on the strategic work of embedding the results in your business and developing appropriate responses.

Whether you are just beginning your CSRD compliance journey or refining your existing approach, we can help you meet the geographic context requirements with confidence.

Ready to get started? Contact us to learn more about how Dunya Analytics can support your ESRS E4 compliance or schedule a demo to see our platform in action.